Securing the Future of Development Finance in a Fragmented World

A roadmap for the 4th International Conference on Financing Development

Development finance is under pressure. Cuts to aid, trade uncertainty, and debt burdens are exacerbating deep vulnerabilities in low-income countries. With the Fourth International Conference on Financing Development (FfD4) set to take place next week, our experts look at how to “future-proof” development finance. They examine the largest sources of development finance and assess their exposure to geopolitical risks, helping prioritize implementation of the FfD4 agenda.

At the end of this month, countries will meet in Seville for the Fourth International Conference on Financing for Development (FfD4), where they will formally adopt an agreement set to shape the global development finance landscape for the next decade.

After more than a year of negotiations, the outcome document was finally agreed on by consensus, —a consensus made possible only after the United States chose to walk away from the process. Their withdrawal cleared the path for a rare agreement among the rest of the international community, lending the text a degree of legitimacy. However, its formation in the absence of a major global actor raises important questions, especially amid mounting global challenges and urgent needs for low-income countries.

The world’s most vulnerable countries grapple with rising debt burdens, climate-related shocks, and capital flight, the impacts of which are compounding in ways that threaten to derail progress on development goals, from building climate resilience to ending extreme poverty.

However, instead of stepping up, many countries have recently stepped back, prioritizing their own national interests rather than working together on global issues. The reduction of official development assistance (ODA) is a sharp demonstration of this, being cut or diverted to domestic priorities. The United States’ withdrawal from multilateral agreements aimed at scaling up development and climate cooperation, including the FfD4 Summit and the United Nations Framework Convention on Tax, reflects the same trend.

This shift has created a political climate where international cooperation tends to settle for the lowest common denominator, focusing on simple, narrow agreements instead of bold, wide-ranging ones. Nevertheless, the consensus reached on the FfD4 outcome document signals that multilateralism, while strained, remains possible, even in a fragmented global landscape.

The challenge now is to leverage this momentum, not just to endorse commitments, but to translate them into action.

Given the current context, the discussions at FfD4 will have to be focused on preventing systemic crises that could derail the whole agenda and pinpointing the key policy moves, both at domestic level and internationally, that can keep progress moving forward, even when crises occur. The outcome needs to be strong enough to withstand the challenges ahead.

By analyzing actual financing flows, including tax revenues, transfers, subsidies, and debt servicing, we can better understand where countries are exposed and what policies offer the greatest leverage. Our analysis breaks down the risks and lays out development finance priorities that countries should focus on.

Geopolitical Risks to Development Finance

1. Cuts to Aid Budgets

ODA is being pulled in multiple directions. As countries grapple with climate finance and humanitarian needs, budgets are shrinking. This is a major blow for low-income countries, as ODA often underwrites essential services and supports macroeconomic stability.

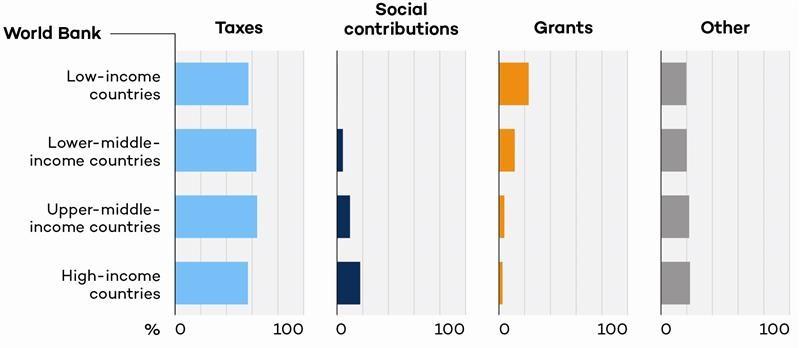

Data shows ODA grants remain critical because many lower-income countries lack social contributions that fund social protection elsewhere, making aid a vital income source.

The issue isn’t just a shortfall in funding. Without predictable ODA flows, countries may turn to more expensive or volatile financing, including commercial debt. This increases fiscal pressure and can lead to a vicious cycle of borrowing.

2. A Fractured Global Trade System

The cut in ODA not only affects capacity to finance public goods, but also the availability of external flows to balance import demand. In lower-income countries, secondary income (current transfers) and capital transfers (project finance) play a significant role in external revenues. As these flows become increasingly scarce, the pressure on exports intensifies.

However, today’s trade system is increasingly unstable. Unilateral tariffs and eroding trust in multilateralism have disrupted supply chains and exposed exporters to more volatility, especially in goods trade, where lower-income countries earn the majority of their export revenues.

For many low-income countries, export revenues remain fragile due to weak tradable sectors, relying heavily on transfers to stabilize external accounts. This exposes them to shocks in political and labour markets globally, increasing vulnerability to trade disruptions.

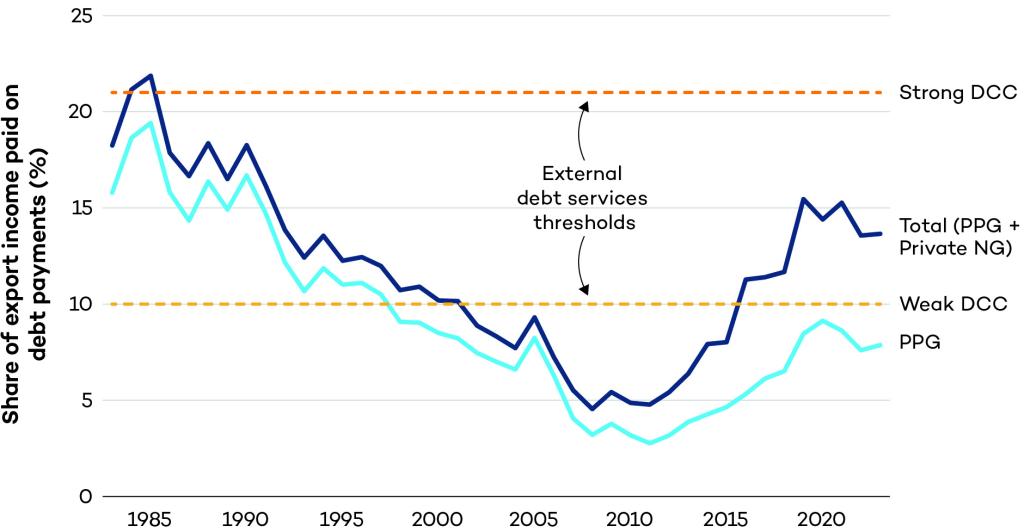

3. A Looming Debt Crisis

External debt vulnerabilities are growing. Many low-income countries now rely on a more complex mix of public, private, and non-concessional debt. This shift, coupled with rising interest rates and falling foreign exchange reserves, has triggered balance of payment pressures in dozens of economies.

Rising exposure to external private debt and more complex creditor mixes risks diverting growing shares of scarce revenues to debt servicing, squeezing public spending on development priorities.

4. Domestic Resource Mobilization Under Pressure

The logical response to falling external finance is to raise more money at home. There’s huge potential to do this—especially through better tax systems—but overreliance on domestic resource mobilization (DRM) is risky.

Without a corresponding boost in external revenues, higher domestic spending could trigger inflation, currency instability, or debt distress.

Taxes remain the largest source of development finance, underpinning domestic budgets. However, data reveals that many countries’ tax systems still miss considerable revenue from wealth and natural resources, while harmful subsidies drain public funds and distort priorities. Social contributions are also underdeveloped, requiring integrated reforms beyond GDP-focused tax efforts.

Six Implementation Priorities After FfD4

The risks outlined above show why future-proofing development finance is critical. As countries adopt the FfD4 agreement, the focus must shift to action that addresses today’s challenges and builds resilience against tomorrow’s shocks.

The six priorities below set out where efforts should concentrate to safeguard progress and strengthen economies for the long term.

1. Reform and Refocus ODA

ODA must be restructured to reflect today’s priorities without double-counting or diluting its core purpose. One approach is to divide ODA into two streams, one focused exclusively on poverty reduction and another dedicated to global public goods like climate action.

A more ambitious proposal would involve a “Beyond ODA” framework, pooling contributions from public, private, and philanthropic sources based on countries’ ability to pay. While politically challenging, even incremental reforms can increase aid effectiveness.

2. Prevent Trade Disruptions from Harming Low-Income Countries

Trade disputes between wealthy nations should not come at the expense of low-income countries. High-income countries must avoid broad tariffs that affect these economies and ensure market access is maintained.

Regional trade integration and South–South cooperation can help diversify markets and reduce vulnerability, but these efforts need support. Stronger trade alliances and fairer trade rules are essential for building resilience.

3. Coordinate Debt Relief Around Balance of Payments Pressures

Debt relief should prioritize easing immediate external financing constraints, not just lowering debt-to-GDP ratios. The focus should be on avoiding economic collapse, supporting investment, and ensuring that relief is timely and adequate.

A deeper reform agenda would involve standardizing sovereign debt restructuring processes across creditor types, from bondholders to multilateral institutions.

4. Strengthen DRM

Three high-impact DRM reforms include:

- taxing wealth and income more effectively: Closing offshore tax loopholes and taxing high-net-worth individuals could generate billions. For example, a 5% tax on EU billionaires could yield over EUR 280 billion annually.

- reforming tax expenditures: Corporate tax breaks cost countries an estimated 4% of GDP globally. These should be rationalized and made transparent.

- expanding natural resource taxation: Countries, especially in Africa, can capture more value from mining and other resource exports, particularly amid the energy transition.

Taxing wealth, rethinking tax incentive strategies, and capturing more from natural resources are three reforms that could help raise much-needed revenues for development.

Social contributions also need attention. Many low-income countries lack universal social protection systems. Closing this gap will require broader development strategies that account for human, social, and environmental well-being, not just GDP growth.

5. End Harmful Subsidies and Expand Green Taxes

Fossil fuel subsidies drain budgets and delay the energy transition. Reforming them—while protecting vulnerable populations—can free up fiscal space and support green development. Additional revenue can be raised through green taxes on carbon, waste, and pollution. These taxes are relatively easy to administer and align with sustainability goals.

6. Promote Export Growth Alongside DRM

DRM must be matched by efforts to boost export earnings. This includes

- diversifying exports beyond a few commodities to reduce volatility

- providing targeted incentives to boost industrial output

- using trade taxes wisely to raise revenue without undermining competitiveness

This complements DRM and reduces the risk of balance of payment crises.

Aid cuts, debt distress, and trade fragmentation have already begun to reshape the financial landscape for low-income countries. Future-proofing the FfD agenda requires anticipating these risks and acting to mitigate them.

At the global level, this means ensuring meaningful debt relief, stabilizing trade access, and redesigning ODA for today’s challenges. At the national level, countries must reform tax systems, scale social protection, invest in export capacity, and phase out harmful subsidies.

However, overloading domestic budgets in low-income countries with more responsibility without international backing is both unfair and unsustainable. A development finance strategy that relies too heavily on DRM alone risks backfiring, destabilizing economies and undermining the very goals it seeks to achieve.

The path forward must be integrated, evidence-based, and politically savvy. Only then can we build resilient, future-ready financing systems that truly support sustainable development.