The conclusion is that Canada’s U.S. export patterns provide a buffer but do not shield it much from lower demand for its exported crude oil as global demand drops.

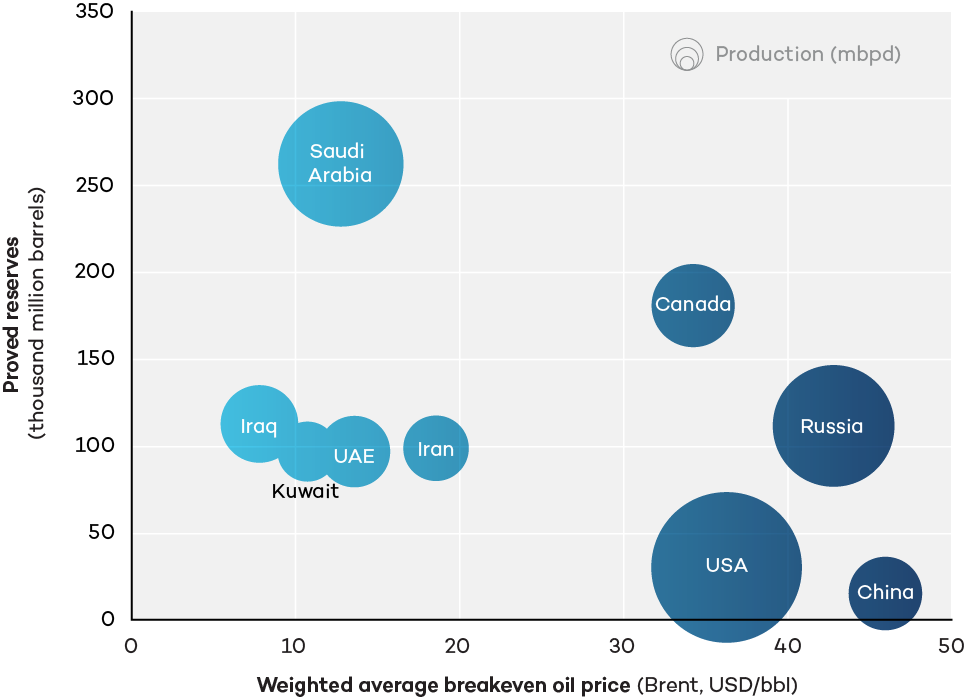

Canada is also directly vulnerable to the price impacts of a global decrease in demand, and its U.S. export markets do little to shield it from those impacts. Prices are, to a large extent, set in a global market. Those prices are set both by demand and supply, however, so it matters what Canada’s global competitors will do as demand falls—a topic that is explored below.

ESG Credentials Will Not Preserve Canadian Oil’s Market Share

If Canada were vying to sell the proverbial last barrel of oil, would it matter how its oil was produced? Would greenhouse gas (GHG) intensity matter, for example, or would it matter whether it was considered “ethical” or produced to high ESG standards? The short answer is: probably not.

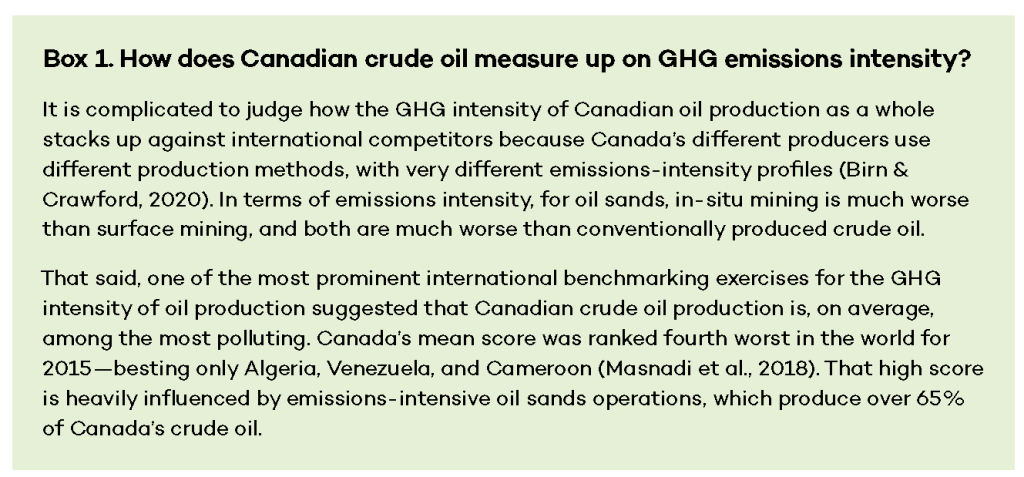

For some products, production methods impact marketability. At comparable price and quality, final consumers will favour “green” and ethically produced products. For goods like food, clothing, and electronics, a variety of labelling schemes allow consumers to choose, even to pay a premium for labelled products. But for commodities like oil, the situation is different. When refined Canadian oil is finally sold at the pumps, it is indistinguishable from other gasoline, and tracking the source at the retail level would be daunting. The original customers are mostly U.S. refiners dependent on the supply of heavy Canadian crude, as detailed above, who focus on quantity, quality, and price—not ESG. ESG considerations clearly matter a great deal to oil sector investors, but they do not preoccupy most customers. While investors influence companies’ ability to finance expansion, new projects, and infrastructure, they don’t buy the final product, and therefore their opinions don’t directly affect a company’s market share. This will be especially true in the context of a shrinking market in which Canadian producers will not need to expand operations to compete for the few remaining buyers. Canadian crude oil’s emissions intensity would matter if the United States implemented a clean fuel standard governing the life-cycle carbon content of transportation fuels such as gasoline. By design, such a standard would reduce the market share of crude oil produced at high emissions intensity, including most of Canada’s U.S. exports (see Box 1). California, Oregon, and Washington have clean fuel standards in place. But, while such a policy has been suggested by legislators, it would face strong opposition from the domestic refining sector and raise the price of gasoline for American drivers, making it unlikely to pass in the foreseeable future.

Beyond the question of whether ESG matters for Canadian oil’s market share is the more basic matter of whether Canada’s producers are, in fact, world leaders on ESG criteria, as claimed by some industry groups and pundits.

On environmental performance, the section above makes it clear that Canada’s overall GHG intensity of production is not world class. Beyond emissions, Canada’s oil sands operations have been dogged for years by a record of serious water and air pollution impacts. Those impacts were singled out as disproportionately affecting Indigenous peoples by the United Nations Special Rapporteur on the implications for human rights of the environmentally sound management and disposal of hazardous substances and wastes.

Oil sands development has been responsible for extensive impacts on the traditional territories of many First Nations in Alberta, in violation of treaty rights and without proper consultation or respect for basic principles such as cumulative effects management. In many instances, the industry’s consultations and impact assessments with respect to Cree, Dene, and Métis rights have been designed in a manner to expedite oil sands development. Members of many Nations in the region, such as Athabasca Chipewyan First Nation and Fort McKay First Nation, have denounced these impacts for decades. Additionally, the Beaver Lake Cree Nation has an ongoing lawsuit against the governments of Alberta and Canada on the basis that the cumulative impacts of this industrial development violate their Treaty 6 rights.