Momentum for a just transition in Canada is building, but to date there remain few public details on the federal government’s concrete plans. As the government moves to develop a sustainable jobs strategy, table just transition legislation, and expand the regional round tables on energy and resources, labour, Indigenous nations, and civil society must be fully involved in the process. Canada’s efforts to ensure workers and communities are supported through the energy transition require partnership with those affected to successfully usher in a swift and fair transition.

In this webinar, we bring together experts from labour, Indigenous, and environmental organizations working on just transition in Canada. Each panellist will share their insights and policy expectations for federal just transition legislation and strategy, with opportunities for collaborative discussion and Q&A.

Speakers

Carolyn Gibson, Natural Resource and Economic Development Policy Advisor, Metis National Council

Ken Bondy, National Representative, Unifor

Vanessa Corkal, Senior Policy Advisor, Canada Energy Transitions, International Institute for Sustainable Development

Alex Callahan, Director of Health, Safety and Environment, Canadian Labour Congress

The Bottom Line: Unpacking the future of Canada's oil & gas

Re-Energizing Canada is a multi-year IISD research project envisioning Canada's future beyond oil and gas. This policy is part three of The Bottom Line series, which digs into the complex questions that will shape Canada's place in future energy markets. (Download PDF)

October 3, 2022

Summary

Energy security stems from energy availability and affordability.

Canada’s energy system is dominated by oil, gas, and coal and is therefore susceptible to the geopolitics of global producers and unpredictable market forces.

The cost of renewable energy has declined to the point where, in many markets, it is less expensive than gas or coal-fired electricity.

Renewable energy prices do not fluctuate with global fuel markets, making them far less susceptible to volatility and price spikes.

Canada is well positioned to manage high amounts of variable renewable energy without compromising reliability.

Electrification of transportation and heating can further protect Canadians from exposure to volatile fossil fuel markets.

Governments should prioritize investments in clean, flexible, and reliable electricity grids to support energy security.

Oil, gas, and coal have been the central pillar of the global energy system throughout the 20th century. And for decades, these fossil fuels have been closely associated with energy security.

The perception of energy security, however, is rapidly changing. Renewables form an increasing share of energy sectors worldwide as countries look to deliver on the Paris Agreement and mitigate the effects of climate change. Moreover, Russia’s invasion of Ukraine has demonstrated how relying on fossil fuels for power, heating, and transport has left many countries vulnerable or energy insecure.

The International Energy Agency (IEA) defines energy security as “the uninterrupted availability of energy sources at an affordable price” (IEA, 2019a). This definition hardly describes today’s global energy situation, with the cancellation of natural gas deliveries and skyrocketing prices for oil and gas products. These circumstances have cascading effects on electricity prices in countries like the United Kingdom that rely heavily on natural gas to produce electricity. In Europe, energy insecurity has been even further amplified since the Russian corporation Gazprom recently cut off gas supplies to several countries.

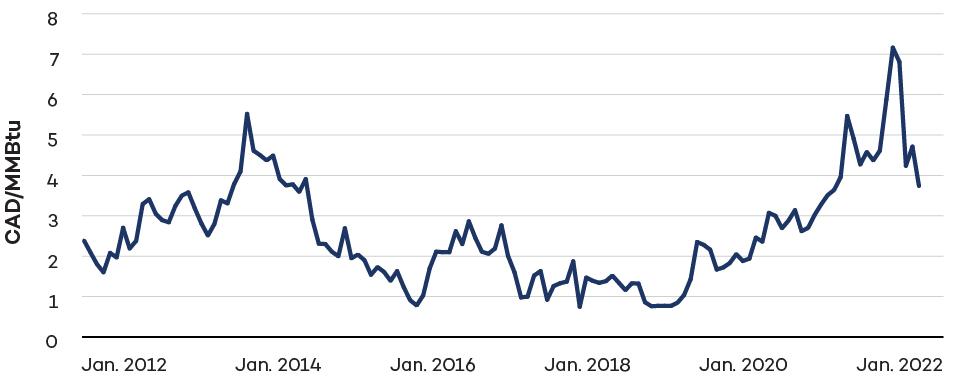

As a result, energy security has gained new urgency in Canada and worldwide. Recent events provide a stark reminder of the volatility and potential vulnerability of global fossil fuel markets and supply chains. Even in Canada, as one of the largest producers of oil and gas in the world, the price of fuels depends on global and regional market forces rather than government policy or market design. Thus, the average monthly price for gasoline in Canada hit a record high of CAD 2.07 per litre in May 2022 (Figure 1), and natural gas prices surged to a record CAD 7.54 per MMBtu in May 2022 (Figure 2).

Energy price increases of this magnitude are more than enough to strain Canadian household budgets. But on top of that, oil and gas prices have accelerated inflation more broadly as it has become more expensive to produce, transport, and store goods, including food and other basic commodities.

Figure 1. Monthly average prices of gasoline in Canada, 2006–2022 (CAD cents/litre)

Figure 2. Alberta Energy Company (AECO) natural gas prices in Canada (CAD/MMBtu)

Source: GLJ, 2021.

Although the dynamics of rapidly transitioning energy systems remain uncertain, renewable energy technologies have the potential to improve energy security by providing uninterrupted and affordable energy in the immediate future.

Oil and Gas Markets Are Inherently Volatile—and Will Continue To Be

The inherent volatility of global fossil fuel markets became painfully evident in 1973 when the world saw its first oil crisis after World War II. The price of oil increased from USD 2.90 per barrel in October to USD 11.65 in January 1974, leading to a global recession. The oil crisis spurred governments worldwide to pursue other energy types, including renewable energy, nuclear, and hydropower, to ensure the security of supply. Most countries also increased efforts to extract fossil fuels domestically. Likewise, coal saw a resurgence, and governments turned to energy-efficiency policies such as car-free Sundays and other consumer-focused measures to curb demand.

Natural gas markets are more regional than oil markets. However, in the last decade, the regional gas markets have become more integrated due to better transportation opportunities and increased trade in liquified natural gas. Despite being more regional, due to market design, consumption patterns, and storage and transportability challenges, natural gas markets have arguably been more volatile than the market for crude oil.

The volatility of natural gas markets has been evident over the last year. Even before the Russian invasion of Ukraine, natural gas market instability was notable, with prices spiking significantly across all markets. In October 2021, record-high gas prices in Europe and Asia associated with the COVID-19 recovery were spilling over into the American market, driving 12-year high prices of USD 6.31 per million Btu. Likewise, implied volatility, a measure of the expected fluctuations of future gas prices, rose to an all-time high of 122.5% in early October. The war in Ukraine exacerbated these trends, leading to record-high prices in the North American market in 2022.

Faced with an energy crisis, the European Union (EU) and member states are doubling down on existing climate commitments and accelerating the transition away from natural gas. EU leaders are calling for more renewable energy to improve energy security: as EU Energy Commissioner Kadri Simson said, “The only long-term remedy against demand shocks and price volatility is a transition to a green energy system”. Similarly, the German Finance Minister has labelled renewable energy the “energy of freedom”, and the Danish government has decided to phase out natural gas completely by 2030 on energy security grounds.

“The only long-term remedy against demand shocks and price volatility is a transition to a green energy system”.

Renewable Energy Is More Affordable

In contrast to oil and gas, renewable energy can reliably deliver affordable energy. This is a unique and positive aspect of today’s energy crisis compared to historical crises: options for electrification and renewable-based electricity systems are both available and cost-effective.

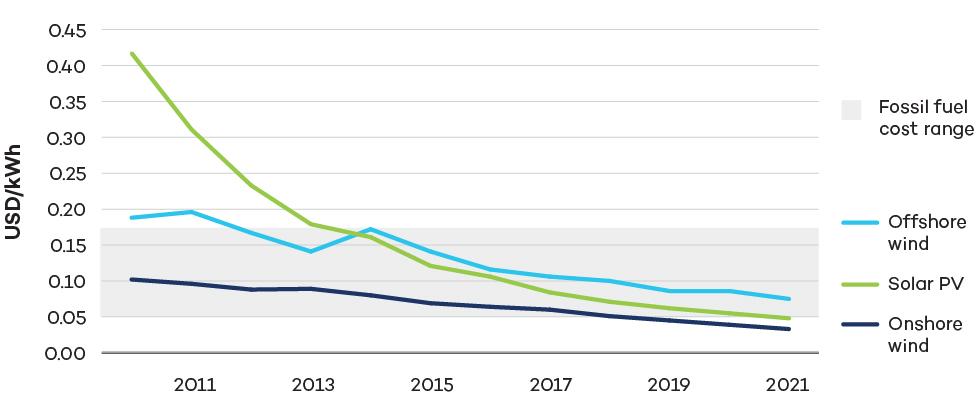

For new power capacity, wind and solar are now cheaper than any other source. According to Equinor, wind and solar were already cheaper than gas-based power in 2020. This means that renewable energy was already the cheaper option for new power before the recent natural gas price spikes. As illustrated in Figure 3, the cost of new renewable energy has dropped so dramatically that, for many countries, it is cheaper to install new solar or wind infrastructure than to keep operating existing fossil fuel-based power plants. This means that replacing fossil-based electricity generation with renewables would save money and reduce emissions. Wind and solar prices are expected to continue their downward trends as more countries increase deployment and learn how to best integrate these sources into the grid.

Figure 3. Levelized cost of electricity (LCOE) for newly commissioned utility-scale solar photovoltaic (PV) and onshore and offshore wind from 2010 to 2021 (USD/KWh)

Source: IRENA, 2022.

The LCOE is a measure of the average net present cost of electricity generation for a generator over its lifetime. LCOE is frequently used to compare the price of different electricity generation options over an asset’s lifetime. Figure 3 shows significant price decreases for renewables over the past decade, with costs declining 88% and 68%, respectively, since 2010 for solar PV and onshore wind. The fossil fuel range illustrates that both solar PV and onshore wind prices are now lower than the cheapest fossil fuel-based alternative by 11% and 38%, respectively. IRENA’s LCOE numbers are based on a global weighted average.

One benefit of an electrified system powered by renewable energy is that it does not rely on input fuel to operate. Once built and connected to the grid, the cost of renewables does not fluctuate based on fuel prices; renewables can then operate at consistent, low costs, which, in turn, can lower electricity prices across the entire system. For instance, when the wind is blowing in Alberta, wholesale electricity prices in the province drop (Independent Power Producers Society of Alberta, 2022). Long-term price stability can also be locked-in through energy purchase agreements that guarantee the price of renewable resources decades into the future.

And finally, renewable energy is either installed (provincially/territorially) or imported regionally through transmission lines. With an electricity system based on renewables, governments can more directly ensure affordable and reliable energy through market design and policy.

Renewable Energy Is Reliable

To deliver on the uninterrupted availability side of the energy security equation, renewable power must remain reliable even as more variable energy sources, like wind and solar, are added to the system. For Canada and other countries to achieve high energy security through electrification, grid system operations must be able to support this.

Canada’s power sector is well placed to perform in all four categories. Canada has more than 160,000 km of transmission network lines, mainly running north to south across the U.S.-Canadian border. In terms of regional electricity connections, Canada has 37 connection lines to the United States and exports around 10% of its total electricity generation. More integration of provincial electricity grids is needed and there remain political, social, and institutional barriers to increasing interprovincial transmission infrastructure, however, interprovincial trade presents a technically feasible and cost-effective means to support increased renewables and improve the resilience of the grid.

Large hydroelectric resources can be operated with flexibility in order to ramp up and down to match changes in electricity supply or demand. Canada’s existing hydroelectricity capacity, which accounts for about 60% of the country’s electricity generation, provides significant flexibility to complement variable resources like wind and solar. In addition, all provinces and territories with a high proportion of fossil fuels on their electricity grids—which are thus prime candidates for a large scaling-up of renewables—are adjacent to provinces and territories with extensive hydroelectric resources that could support them. Additionally, provinces with existing large hydroelectric resources benefit greatly from purchasing low-cost renewable electricity from neighbouring regions, and shifting the use of more expensive hydro to when it’s needed.

Storage technologies are another means to improve the flexibility of the grid. Like renewables, the costs of utility-scale lithium-ion batteries are falling rapidly and are projected to continue to decrease, in part due to innovation in transportation applications.

Forecasting is also well advanced, with regions using 12-hour power forecasts that are updated every 10 minutes. As wind and solar capacity in the power system increases, forecasting will improve based on the analysis of historical data from installed sources.

The integration challenge has already been solved in European countries with high shares of variable renewable resources. In Denmark, the security of supply is 99.997% (the highest in Europe), with 50% of all power coming from wind. Moreover, forecasting and the reliability of wind power are so advanced that it is part of the capacity market for manual reserves, which means that variable renewable energy is considered as reliable as thermal power plants based on biomass or coal.

Renewables Can Provide Energy Security to Canadians

In Canada, gas-generated power accounts for 11% of total electricity production. Refined petroleum products and natural gas use account for 76% of total end-user demand across the country, including for transport and heating. Therefore, most of the energy that Canadians use is priced based on markets that are outside of Canadian control. As the current energy crisis shows, global price mechanisms for fossil fuels provide no shelter for Canadian consumers, even though Canada is a major oil and gas producer. Nevertheless, Canada is well placed to bolster its energy security by supporting electrification and renewable energy.

Clean electricity grids are well within reach across the country. Canada is already a global leader in the power sector, with 82% of its electricity coming from non-emitting sources, mainly hydropower. Legacy hydroelectric development has been bolstered by coal phase-outs, implemented first by Ontario and Alberta and followed by a federal regulation ensuring a nationwide phase-out by 2030. More recently, the federal government has committed to a non-emitting electricity grid by 2035 and developing clean electricity regulations to meet that end. Detailed modelling has shown how Canada can meet its 2035 target, support increased electrification, and provide reliable, affordable electricity across the country by prioritizing wind, solar, electricity storage, and additional interprovincial transmission. This scenario is modelled with no new nuclear or natural gas generation.

Expanding renewables is also a cost-effective option. Electricity prices across the country demonstrate that provinces and territories with high shares of renewable energy have been able to keep power prices low with renewable electricity production. Households in fossil fuel-reliant provinces such as Saskatchewan pay 60% more for their power than households in Quebec and 45% more than households in Manitoba. Although the cost differential is related to legacy hydroelectric development, the falling costs of solar, wind, and battery technology mean that these sources provide the lowest cost options for supplementing existing hydroelectricity or replacing coal and gas power generation.

Information from the Alberta Electric System Operator confirms that wind and solar are already the cheaper options for new power than gas (normally the cheapest fossil fuel-based alternative). This shift is also evident when looking at actual power sector development in Alberta in recent years. In its deregulated and competitive market, Alberta added a remarkable 1.6 GW from wind and solar between 2019 and 2021, resulting in wind and solar accounting for 17% of total capacity in 2021. At the same time, the province has phased out coal faster than expected.

Modelling in Alberta, New Brunswick, and Nova Scotia has also shown that clean energy portfolios, including wind, solar, battery storage, demand flexibility, and energy efficiency, can provide the same grid services as natural gas generation at a lower cost.

As noted above, more flexible electricity grids will be needed to support renewables. This flexibility will include more integrated provincial and territorial grids that maximize renewable energy sources across the country. Currently, Canadian provinces are better connected to the United States than to each other. Provinces and territories need to improve connectivity so that Canada can benefit from their different strengths—from plentiful hydropower in some provinces and territories to the enormous potential for wind and solar in others. Additional investments and regulatory reforms are necessary to ensure adequate storage and “smarter” grids that support improved forecasting of supply and demand and that fully enable demand management.

Reducing Demand for Fossil Fuels Increases Energy Security

While renewables and storage technologies can eliminate fossil fuels from the electricity grid, electrifying end uses and reducing demand through energy efficiency will limit Canadians’ direct exposure to fluctuating fossil fuel prices. At the household level, electricity currently accounts for 23% of energy use. However, that is predicted to grow to 96% in 2050 if Canada achieves its net-zero target.

While this transition is already underway, accelerating the phase-out of fossil fuels in household consumption will improve energy security, in part because sectors such as personal transport and heating, where demand for fossil fuels is high, have readily available, cost-competitive alternatives.

The federal government’s target of no new combustion engine vehicles as of 2035 is a policy step that will not only help Canada build a cleaner future but also help to considerably reduce its dependency on oil and gas. Canada has more than 25 million light-duty vehicles on the road, and to reach the 2035 target, the government is aiming for 60% of new sales to be zero-emission vehicles by 2030. However, it has been noted that the market for electric vehicles is now established to the point where market dynamics are replacing government policy as the key driver for adoption.

Other demand-side policies could include efforts in Canada’s building sector, where gas plays a key role. About a quarter of Canada’s final energy consumption comes from buildings, with 65% going to heating and cooling (IEA, 2019a). Choosing high-efficiency electric heat pumps for heating and cooling and investing in deep energy retrofits will help reduce Canadians’ exposure to volatile natural gas prices while reducing emissions and improving the comfort of homes.

The electrification of buildings and transport will create additional demand for electricity requiring 2.2 to 3.4 times more electricity capacity in 2050. However, detailed modelling shows how this increased demand can be reliably met with wind, solar, energy storage, and interprovincial transmission.

Renewables and Electrification Are Key to Energy Security

Canada is a leading producer of oil and gas. However, systems that rely on fossil fuels to operate will continue, throughout their lifetime, to be subject to volatile market forces, supply chain disruptions, and geopolitics. This volatility is a risk to energy security because it means that Canadian governments, both provincial and federal, have little recourse to ensure that affordable and reliable energy supplies are available.

Fortunately, the transition to an electrified system based on renewables has already begun, and cost-competitive, clean alternatives to oil, gas, and coal are available. The costs of wind, solar, and battery storage technologies are rapidly declining, and experience shows how grids can support significant amounts of variable renewables while maintaining reliability. At the same time, the electrification of transport, heating, and cooling are poised for major gains.

Limiting the effects of climate change has been a driver for electrification and the deployment of renewables. However, energy security provides a rationale to accelerate the transition. Although the amount of electricity that households use will increase, overall energy costs are projected to decrease. Since renewables do not require input fuels, their operational costs are both low and predictable. Completing the transition will require planning and investment. In particular, governments need to ensure that regulatory reform, market design, and investment in grid infrastructure enhance the flexibility and resilience of electricity grids. In addition, it will be necessary to ensure that access to clean, affordable energy services—including energy efficiency options—is available to Canadians in all regions and income levels.

Nevertheless, renewables and electrification are the best options to increase Canada’s energy security, particularly the long-term affordability of supply. For the first time in history, governments have the tools to address the systemic problems with oil and gas that an energy crisis has once again laid bare—Canada now needs all hands on deck to seize the opportunity and reap the benefits.

Re-Energizing Canada is a multi-year IISD research project envisioning Canada's future beyond oil and gas. This publication is part three of The Bottom Line policy brief series, which digs into the complex questions that will shape Canada's place in future energy markets.

Canada’s West Coast can export LNG globally, but East Coast faces pipeline constraints, TC Energy CEO says

Canada's West Coast is positioned to become a reliable supplier of liquefied natural gas, but the East Coast faces pipeline constraints, says TC Energy Corp.'s chief executive officer.

Indigenous-led Cedar LNG seeks regulatory approval under new climate rules

Cedar LNG, an Indigenous-led project in British Columbia, is hoping to become one of the first energy proposals in Canada to win approval in a new regulatory process that is designed to pay greater scrutiny to climate impacts.

Why Canada Needs to Plan for a Steep Decline in Global Oil Demand

The Bottom Line: Unpacking the future of Canada's oil & gas

Re-Energizing Canada is a multi-year IISD research project envisioning Canada's future beyond oil and gas. This policy brief is part two of The Bottom Line series, which digs into the complex questions that will shape Canada's place in future energy markets. (Download PDF)

September 16, 2022

Summary

International Energy Agency scenarios project a decline in oil demand globally as climate policies intensify.

Canada’s own energy body, the Canada Energy Regulator, shows a projected decline in Canadian production.

Decline in oil demand is driven primarily by road transport, the largest component of crude oil demand at 44%, with the electrification of passenger vehicles especially leading the way.

Other end uses for oil will reduce demand post-2030 or earlier under aggressive policy scenarios.

Trends suggest global demand for oil will be in decline by 2030 and will drop significantly thereafter.

What is the future of global demand for oil? This is a critically important question for Canada as the global energy transition gains momentum, and governments establish policies to limit greenhouse gas (GHG) emissions, support economic stability, and promote energy security. To limit warming to 1.5°C, the world’s economy must quickly move away from fossil fuel consumption and reduce demand significantly, and trends in policies and technologies suggest this transition is already underway. This means that Canada, as a major oil exporter, will have to contend with a shrinking global market post-2030.

This brief will make the case for a near future with much less global demand for oil. Future briefs in this series will explore what this means specifically for Canadian producers.

Climate Action Continues to Build Momentum That Is Reflected in Future Oil Demand Scenarios

To understand potential future demand for oil, it is useful to consider both international and domestic analyses. Two influential analyses of possible futures for oil are annually delivered by the International Energy Agency (IEA) and the Canada Energy Regulator (CER). While only these two outlooks are discussed in this brief, as the most relevant and authoritative, they are in line with the many other credible analyses that predict a peak of global oil demand by 2030 or earlier.

Stated Policies Scenario (STEPS)—A low climate-ambition scenario that assumes only current energy-related climate policies and those in progress will be adopted between now and 2050, with no ratcheting up of plans or targets.

Announced Pledges Scenario (APS)—This scenario assumes the energy-related climate targets made by governments as of 2021 are achieved by 2050, even if policies to achieve these targets are not yet in place.

Net-Zero (NZE)—A more ambitious scenario where the global energy sector reaches net-zero GHG emissions by 2050, via a hypothetical set of government policies and behavioural changes. This is the only IEA scenario that is consistent with limiting global warming to 1.5°C.

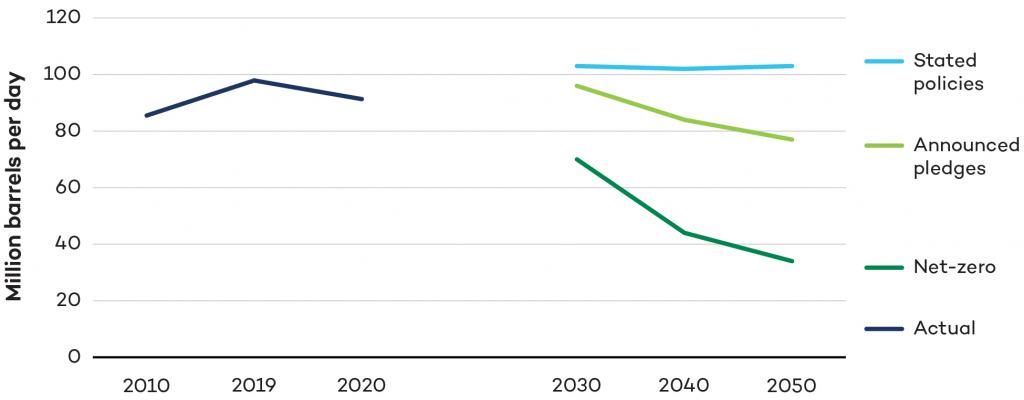

Figure 1. WEO 2021 global oil demand

Source: International Energy Agency, 2021.

As shown in Figure 1, in the STEPS, demand for oil rebounds in the near term to pre-COVID levels, increases slightly out to the 2030s, and stays more or less stable at 103 million barrels per day (mbpd) to 2050. By contrast, in the APS, demand peaks around 2025 and falls by 1 mbpd per year between 2030 and 2050. In the NZE, oil demand has already peaked. It falls to 70 mbpd by 2030 and by 2.4 mbpd (or 5.3%) per year thereafter to 2050.

The CER’s Canada’s Energy Future 2021 also produces scenarios on the future of oil, but these are different from the IEA scenarios; they describe future production of Canadian oil given projected oil prices rather than future demand. They are not based on the same depth of global policy and technology analysis that is used by the IEA. At present, the CER does not model a scenario that is consistent with limiting global warming to 1.5°C. In 2021, the CER modelled two scenarios that cover Canadian crude oil production:

Current Policies Scenario—This scenario assumes future energy-related climate policy remains unchanged from what is in place at the time of modelling. There is some technological improvement in mature technologies but limited uptake.

Evolving Policies Scenario—This scenario assumes global energy-related climate policies are expanded at the same pace as they have been in recent years. Policies in development are adopted, and existing policies are somewhat strengthened over time. This scenario assumes technological innovation and uptake.

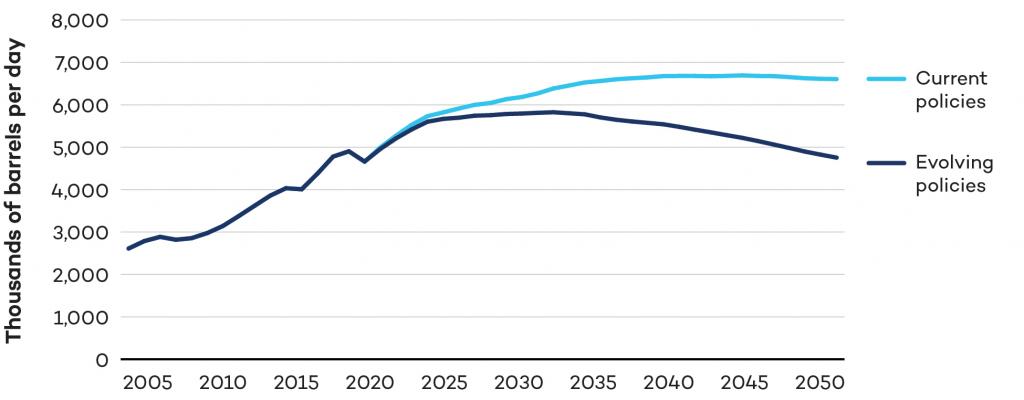

In the Current Policies Scenario, as shown in Figure 2, Canadian crude oil production is projected to rise until 2043 before falling slightly out to 2050. In the Evolving Policies Scenario, production climbs from pre-pandemic levels by 19% to peak in 2032, falling thereafter by an average annual rate of 1.1%, to reach roughly 2018 levels by 2050.

Figure 2. Total crude oil production – CER 2021

Source: Canada Energy Regulator, 2021.

In the analysis that follows, the CER scenarios are not used as a basis for demand forecast; as noted above, that is not what they are intended for. They are shown here to illustrate that even under the CER’s relatively unambitious Evolving Policies Scenario assumptions, oil production in Canada will peak shortly after 2030.

Implications of IEA and CER Scenarios

The various scenarios from the IEA and CER paint very different pictures of the future, with corresponding implications for climate change outcomes and the Canadian oil and gas sector. To plan for economic resilience, it is paramount to assess which of those pictures is most likely.

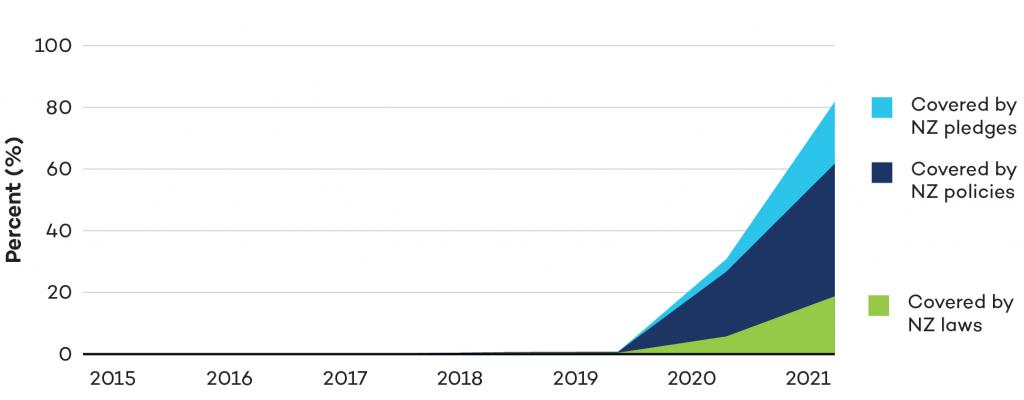

Figure 3. Global GDP covered by NZ laws/policies/pledges

Source: Net Zero Tracker, 2022.

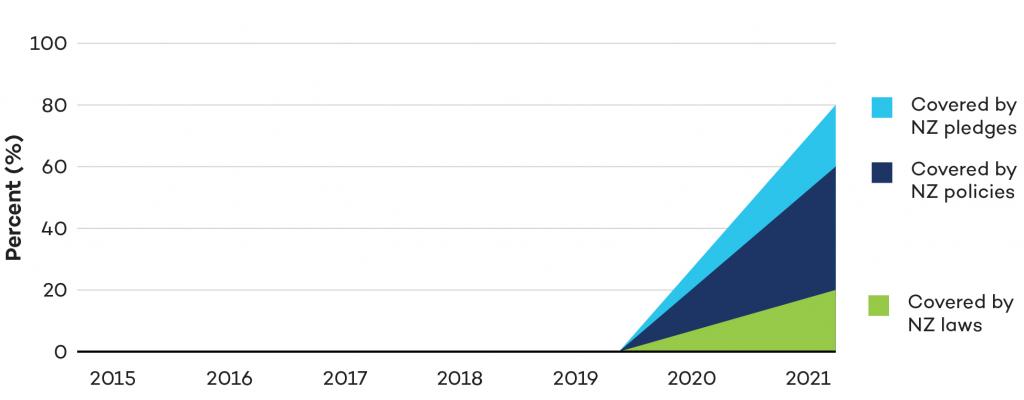

Figure 4. Global emissions covered by NZ laws/policies/pledges

Source: Net Zero Tracker, 2022.

Some scenarios are easily eliminated. The IEA’s STEPS and the CER’s Current Policies Scenario both assume no evolution of existing or in-process climate policies from those that exist today out to 2050. That is so unlikely as to be effectively impossible. Since 2019, there has been a significant increase in national commitments to achieve net-zero GHG emissions. Figures 3 and 4 show a sharp increase in demonstrated commitments to stronger climate policy, with an increasing number of countries—including Canada—putting those commitments into law.

There are three drivers fuelling the trend of strengthened climate policies:

More frequent and powerful physical impacts of climate change the world over, such as heat waves, floods, storm surges, droughts, and wildfires. Compare the last 20 years with the 20 years previous: climate-related disasters (6,681 vs. 3,656); major recorded disaster events (7,348 vs. 4,212); people affected (4.2 billion vs 3.25 billion); and global economic losses (USD 2.97 trillion vs. USD 1.63 trillion). These occurrences also augment public acceptance of the science.

As a result of both those drivers, growing pressure on governments to take action to mitigate climate change.

As atmospheric concentrations of GHGs grow, these drivers will only strengthen. The inevitable policy response means that the only plausible scenarios are those that show either a near-term peak in global oil demand (IEA APS, NZE) or that show Canadian production peaking in 2032 (CER Evolving Policies).

Trends Show Declining Demand for Oil

There is still variability in the remaining scenarios, driven by different assumptions about technology uptake and government policy responses to climate change. To assess the likelihood of the remaining scenarios, it is instructive to consider the major end uses for crude oil and the policies, trends, and technologies that are likely to affect each of them. We examine each in turn below.

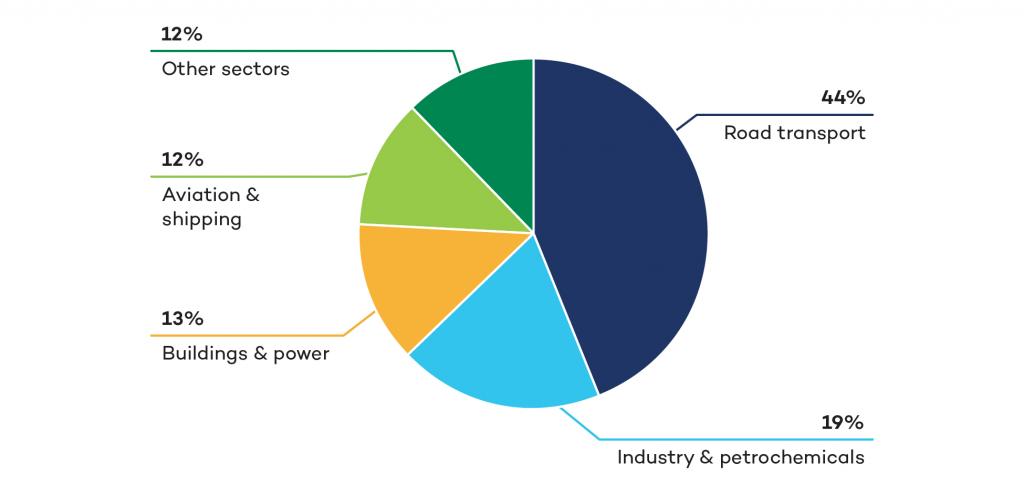

Road Transport

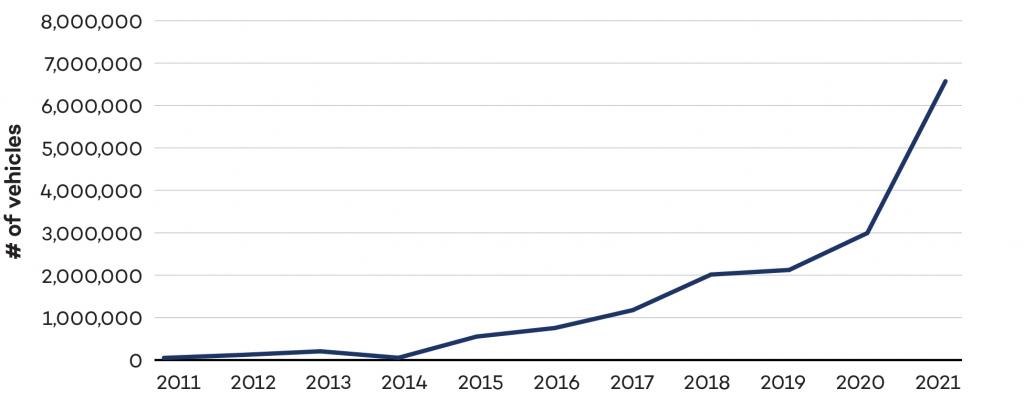

Road transport represents the largest share of demand for crude oil, at 44% (Figure 5) with the pace of transport electrification the most significant factor in determining future demand for oil. Figures 6 to 9 show that the electrification trend in the transport sector is gathering pace with electric vehicle (EV) sales, deployment of charging infrastructure, and battery range (as a proxy for technological development) all showing accelerating trends. In the case of passenger cars, it is easy to envision that in the next decade there will be a sharply reduced market for internal combustion engine vehicles.

The steep rate of change is being driven by evolving government policy. Governments covering 25% of the global market have announced 100% EV sales mandates for 2035, and EV-related subsidies doubled in 2021 to nearly USD 30 billion. These kinds of policies are low-hanging policy fruit for the many governments looking for ways to address climate change. They can be combined with popular industrial subsidies aimed at fostering competitive firms in the green markets of the future and employment-creating spending on charging infrastructure.

Figure 5. Global demand for oil

Source: International Energy Agency, 2019.

As a result, consumer uptake is poised to hit significant tipping points well before 2035, triggered by several factors, including the increasing affordability of electric vehicles. Under most assumptions, EVs are already cheaper on a lifetime basis or even straight off the lot if financed. Upfront cost parity is expected to come in the mid-2020s. Increasing range, the availability of infrastructure, and growing consumer confidence that comes from familiarity with the technology will also drive EV uptake.

According to Bloomberg NEF, “The market is shifting from being driven primarily by policy, to one where organic consumer demand is the most important factor. As regulatory drivers begin to play less of a role, consumer adoption dynamics—the ‘S-curve’—take over”. The S-curve describes the uptake of new technology that eventually takes off not in a linear fashion but exponentially, with sudden and overwhelming effects (Foster, 1986). There are numerous examples of such a dynamic with past technologies, including cellphones, personal computers and, ironically, internal combustion engine passenger vehicles.

Another driver of S-curve adoption rates will be the reluctance of new car buyers to purchase a conventional vehicle that they see as having low resale value—a positive feedback effect that will intensify as the market share of EVs climbs. EVs may also play an outsized role in the destruction of demand for oil well beyond their market share. Fleet owners, taxis, and ride-hailing services will be early adopters of EVs, given lifetime cost considerations, and their vehicles are driven many more kilometres than the average. Owners of multiple vehicles will likely also prefer to use the EVs over conventional vehicles if they have a choice, given the significant difference in operating costs.

To be on track with the IEA’s Net-Zero scenario, 64% of passenger car sales and 5% of truck sales would have to be electric by 2030. The above trends suggest that this trajectory is within range.

The outlook for uptake in heavy-duty vehicles (HDVs) is not as straightforward, as there would need to be large investments in highway charging infrastructure. However, policy and technological developments for HDVs have been accelerating, with China as an important early adopter. EVs for medium-duty trucks on urban duty cycles as commercial vehicles are already the cheapest option for many users, and face few infrastructure challenges.

Figure 6. Global EV sales (Light-Duty Vehicles)

Source: International Energy Agency, 2022.

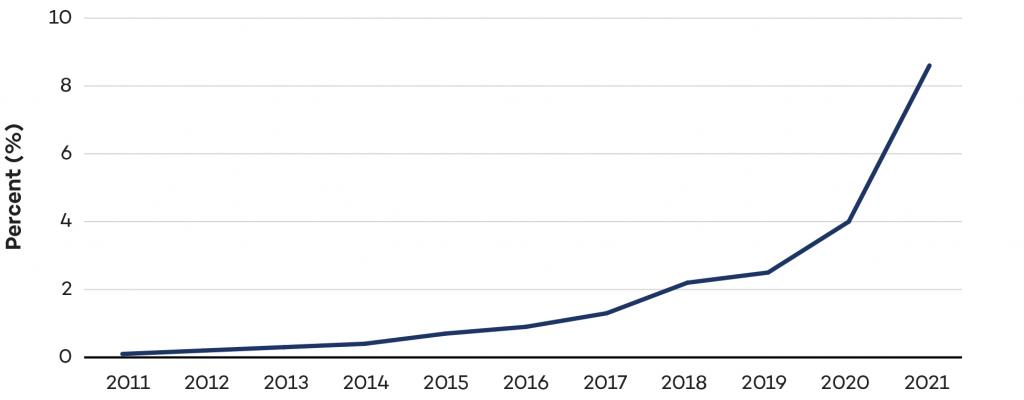

Figure 7. Global EV sales share (Light-Duty Vehicles)

Source: International Energy Agency, 2022.

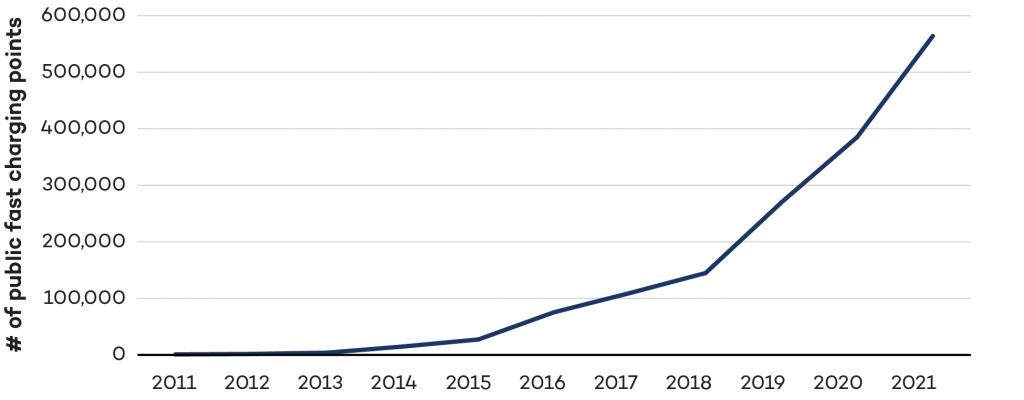

Figure 8. Global EV public fast charging points

Source: International Energy Agency, 2022.

From the perspective of road transport—the biggest factor in oil demand—the trends are tracking toward the IEA’s Net-Zero scenario. This would mean a significant displacement of oil demand beginning before 2030 and picking up pace as the share of electric vehicles grows exponentially. Compared to the business-as-usual Stated Policies scenario, the Net-Zero Scenario implies a drop in the demand for oil needed for road transport of 18.8 mbpd by 2030 and 49.9 mbpd by 2050.

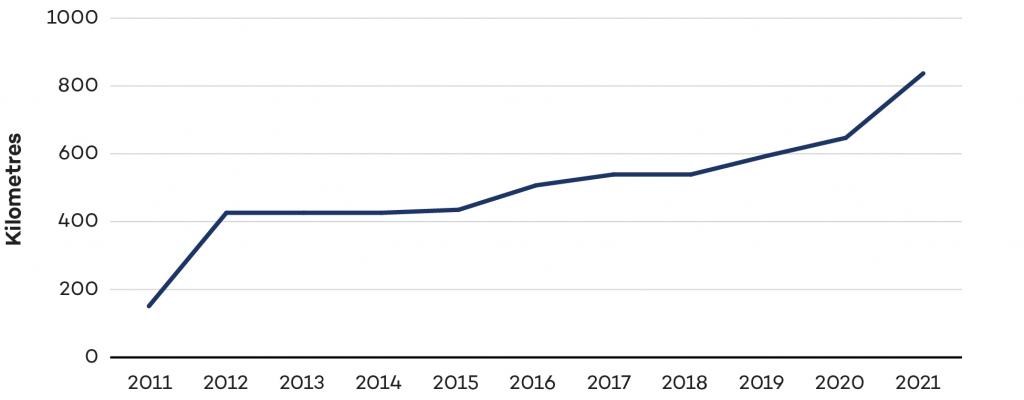

Figure 9. Maximum range (U.S. EV models)

Source: United States Department of Energy, 2021.

Plastics

Industry and petrochemicals make up the second largest share of demand for crude oil globally at 19%. Oil is a feedstock to the petrochemical industry, which uses it to produce a wide range of plastic products (though in North America the more common feedstock is natural gas). Demand destruction in this sector would come from policies aimed at reducing plastic pollution.

The IEA scenarios do not predict such policies will have a major impact on oil demand out to 2050. The IEA calculates petrochemicals’ share of growth to be 50% by 2050 on current trajectories. BP’s assumption is even higher, at 95%. This is based on assumptions about economic growth in developing countries and their catching up with OECD rates of plastic consumption, though others argue that developing country uptake will not mirror historical patterns in developed countries.

Measures such as bans on single-use plastics, now in force in a slew of countries, only nibble at the edges of demand, but a global ban would reduce petrochemical-related oil demand by more than a quarter. Aggressive recycling policy and legislation could lead to more significant impacts, reducing annual growth in oil demand by up to 1% by 2040 or the possibility of peak plastic demand by 2027.

There is growing momentum behind regulatory policies to reduce plastic use more broadly and accelerate recycling. For example, a new multilateral environmental agreement on plastics is progressing quickly. The resulting multilateral agreement is expected to facilitate national commitments and actions in the same way that the United Nations Framework Convention on Climate Change and its Paris Agreement do for climate change. Critically, the scope of talks includes considering measures along the entire life cycle of plastics, including production restrictions.

The IEA’s Net-Zero scenario requires an increase in plastics recycling rates globally, from 17% to 27%, by 2030, and even that would fail to completely avoid an increase in oil demand for the sector—predicted at 1.5 mbpd. But while reduction in plastics demand in the near term may only marginally affect oil demand, the strong rise in multilateral and national regulatory efforts to reduce plastics pollution is likely to have significant impacts post-2030.

Aviation and Shipping

Policies and technologies are not as advanced in the area of aviation and shipping, which accounts for 12% of final demand for crude oil globally. However, policy responses are beginning to take shape. In aviation, 2021 brought a flurry of net-zero pledges from major global carriers and associations. In the same year, 28 states signed on to the International Aviation Climate Ambition Coalition (COP 26 declaration, 2022), committing to a pathway consistent with the Paris Agreement 1.5°C target, and the U.S. Federal Aviation Authority (2021) committed to net-zero by 2050. Proposed mandates such as ReFuel EU and the United Kingdom’s Jet Zero Consultation will act as drivers of cost reduction and uptake for sustainable aviation fuel, which will eventually anchor emission reductions in long-haul flights. For short-haul flights, alternatives have advanced enough that Sweden and Denmark have announced that all domestic flights will be fossil fuel-free by 2030, with Norway aiming for 2040.

While the shipping sector is not likely to contribute to a significant displacement of oil demand between now and 2030, a revision to the International Convention for the Prevention of Pollution from Ships comes into effect in November 2022, requiring all ships to meet annual ship-specific targets to reduce their carbon intensities—a measure that could cut emissions 11% over 2019 levels by 2026 in a full-compliance scenario (Brooks & Adler, 2021). As well, frustration with the International Maritime Organization’s lack of action is spurring national-level efforts that may have significant impacts, including the European Union's proposal to include shipping in its emissions trading system and legislative proposals in the United States to mandate low carbon intensity for ships docking at U.S. ports (Clean Shipping Act of 2022).

Buildings and Power

Buildings, where oil is used for heating, and power, where oil is used to generate electricity, account for 13% of global oil demand, split fairly evenly between the two. For both end uses, oil has alternatives that are, in most cases, cheaper and cleaner, and even the IEA’s most conservative Stated Policies scenario shows demand for both uses falling by 2030.

Relative to 2020 global demand of 91.3 mbpd, these two sectors show a combined drop in demand of 2.7 mbpd by 2030 in the Announced Policies scenario, or 5.8 mbpd in the Net-Zero scenario.

These are small but significant reductions in global demand that, like the impacts of transport electrification, would manifest in the near term, that is, by 2030.

Global Demand for Oil Will Be in Decline by 2030

Comparing the IEA’s scenarios against observed trends suggests global demand for oil will peak before 2030 and thereafter decline. Similar conclusions have been drawn by other independentanalysts, and, in the same vein, the CER’s only plausible scenario shows Canadian production peaking in 2032.

Demand reduction will be driven primarily by road transportation, which accounts for 44% of oil demand. Trends in climate policies, technological improvements, and consumer behaviour suggest demand reduction in line with the IEA’s NZE. These will begin before 2030 and will accelerate thereafter.

For other drivers of demand, it is less certain whether trends will bring us closer to the APS or NZE. In either scenario, buildings and electricity, accounting for 13% of global oil demand, will contribute to demand destruction by 2030, dropping by 3.2 mbpd even in the more conservative APS.

The other major elements of global oil demand—plastics, aviation, and shipping, at 31%—are less likely to achieve the IEA’s NZE conditions by 2030. But in the medium term (post-2030), all of them are likely to contribute significantly to falling demand.

If we assumed the IEA’s NZE trajectory for road transport out to 2030 as argued above, and its more conservative APS trajectory for the other elements of global oil demand whose paths are less certain, the result would be a drop in oil demand from pre-COVID (2019) levels of 22 mbpd, or 22%. These same assumptions carried out to 2050 would reduce demand for oil by 57 mbpd, or 58%, even without assuming any of the trends in aviation, shipping, or plastics lead to more destruction of demand than currently announced policies. To put those numbers in perspective, the drop in global demand that devastated oil markets and sent prices for Western Texas Intermediate briefly negative in 2020 amounted to less than 7 mbpd (though that was more abrupt than the changes envisioned here).

Overall, the data suggests that structural changes in road transport will permanently cause a sustained decline in oil demand in the very near term. Post-2030, this will be compounded by reduced oil demand for other key uses. What this means for Canadian producers specifically is not straightforward and will be assessed in future installments of The Bottom Line policy brief series. But the inescapable starting point for Canadian energy policy is clear: global demand for oil will soon unravel in an unprecedented fashion and will not recover.

Re-Energizing Canada is a multi-year IISD research project envisioning Canada's future beyond oil and gas. This publication is part two of The Bottom Line policy brief series, which digs into the complex questions that will shape Canada's place in future energy markets.

New coalition calls for targets to reduce risk of floods, wildfires and heat waves in Canada

Climate Proof Canada makes the recommendations just as the federal Liberal government is expected to release a climate adaptation strategy before the next international climate conference in Egypt in November.

New Initiative to Boost Natural Infrastructure for Communities across Canada’s Prairies to Launch Tomorrow

September 14, 2022

WINNIPEG, Sep 14, 2022—A new 5-year initiative to scale up natural infrastructure in Alberta, Saskatchewan, and Manitoba to ensure cleaner water and resilient communities launches tomorrow.

Natural Infrastructure for Water Solutions (NIWS), an initiative of the International Institute for Sustainable Development (IISD), aims to tackle the growing water challenges facing the Prairies through the power of natural infrastructure.

A virtual launch event on September 15, 2022, at 10:00 a.m. (CST) will explore the future of natural infrastructure and water management across the Prairies and feature remarks from Terry Duguid, M.P., Parliamentary Secretary to the Minister of Environment and Climate Change, and a panel discussion with experts.

NIWS focuses on the need to make a stronger business case for natural infrastructure by demonstrating how impactful and cost-effective it can be. It will also encourage local municipalities to adopt more natural infrastructure projects,enable access to funding for those who want to implement natural infrastructure, and make sure natural infrastructure is supported and championed by all levels of government through policy.

“For us, thriving communities are places where people have access to clean, fresh water; can depend on reliable and sustainable infrastructure year-round; and are protected from the ever-increasing impacts of climate change,” said Richard Florizone, President and CEO, International Institute for Sustainable Development, who will announce the new initiative during the virtual launch tomorrow.

“And we have an answer: natural infrastructure—which involves planning and building with nature to meet our growing infrastructure needs.”

“That’s why—building on IISD’s strong legacy championing natural infrastructure solutions over multiple decades—NIWS brings together partners to look at ways in which natural infrastructure can help meet the water needs of local communities,” said Florizone.

Natural infrastructure is a way to plan and build with nature to meet our infrastructure needs.

It is managed to provide specific infrastructure benefits, with the potential for many other social and environmental benefits. There is increasing evidence that natural infrastructure can deliver much-needed water outcomes cost-efficiently while also providing areas for recreation and habitat to support wildlife, as well as improving the overall resilience of our communities.

Examples range from wetlands to stormwater parks to green roofs.

IISD's work on water and natural infrastructure is funded by multiple sources, including support for the NIWS initiative from the BHP Foundation.

-30-

For more information, or to arrange an interview with an expert about NIWS, please contact: Sumeep Bath,

Editorial and Communications Manager, IISD Experimental Lakes Area

Faute de preuve : La nouvelle Stratégie nationale d'adaptation du Canada doit protéger les Canadiens des effets des changements climatiques

La Stratégie nationale d'adaptation du Canada devrait être finalisée au cours des prochaines semaines et dévoilée avant la conférence internationale sur les changements climatiques COP 27. Bien qu'elle promette d'être un grand pas en avant dans la protection des Canadiens contre les répercussions croissantes des changements climatiques, sans objectifs à court terme ni mesures pour nous préparer contre l'intensification des inondations, des feux incontrôlés et de la canicule à laquelle nous sommes déjà confrontés, ce sera trop peu, trop tard.

Local student wins prestigious international award

A Grade 12 student from Sarnia’s St. Patrick’s High School has won the top prize at an international water awards ceremony in Stockholm. Annabelle Rayson represented Canada on Tuesday by receiving the prestigious 2022 Stockholm Junior Water Prize.

Sarnia student's science fair entry wins international prize

A Sarnia high school student has won top prize at an international science fair competition. Annabelle Rayson, a Grade 12 student at St. Patrick’s Catholic high school, was named the winner among 36 international entries at this year’s Stockholm Junior Water Prize Awards for her project, which was also a winner at the Canada-wide Science Fair and Lambton County Science Fair.