Comprehensive Wealth in Canada

Measuring What Matters in the Long Run

Canadians are Concerned About the Future — and Rightly So

Canadians enjoy levels of well-being that are the envy of much of the world. But is that well-being sustainable? Will our children and grandchildren do just as well as us?

Most Canadians think not.

In a 2018 Environics poll, nearly half (48 per cent) of Canadians reported being basically pessimistic about the direction of the world. In another 2018 poll, the U.S.-based Pew Research Center found that 67 per cent of Canadians said they believed their children would be financially worse off than them.

Short-term indicators like gross domestic product (GDP) are insufficient for measuring sustainability. This is a fact noted by G7 leaders in the communiqué from their 2018 summit in Charlevoix, Quebec. The heads of state of the world’s leading economies said that countries must begin to compile measures that focus on long-term prosperity and well-being.

GDP measures income today. But what matters in the long run is wealth, the foundation of income in the future. More specifically, a country’s produced, natural, human, financial and social capital determine its prospects for the future.

(Read full report or continue to highlights)

Includes stocks, bonds, bank

deposits and other financial

assets owned by households,

businesses and governments.

The value of the skills and knowledge bound up in the people that make up the workforce as represented by lifetime earning potential.

The forests, lakes, minerals, fossil fuels, land and other elements that make up the natural environment.

The buildings, machinery and infrastructure owned by households, businesses and governments.

Measures the degree of civic engagement and trust/cooperation among the members of society.

Together, these five types of capital make up what is known as the comprehensive wealth portfolio. Comprehensive wealth is the foundation for producing all the goods and services—both market and non-market—needed to support well-being. For well-being to be sustainable, comprehensive wealth must be stable or growing over time on a per capita basis. If it is not, the country is eroding its productive base, living off its inheritance rather than building for the future.

This report provides the most complete analysis of comprehensive wealth ever undertaken in Canada and one of the only such analyses undertaken for any country. Based on data from Statistics Canada and other reliable sources, the International Institute for Sustainable Development looked at the evolution of comprehensive wealth from 1980 to 2015.

Our findings suggest Canadians’ concerns for the future are justified. Despite robust GDP growth since 1980, the foundation of this growth—Canada’s comprehensive wealth—has developed much more slowly and is showing real signs of fragility.

What We Found

Overall, our analysis points to four main areas of concern in Canada’s comprehensive wealth portfolio, each of which is a threat to long-term prosperity and well-being.

1. Slow Growth in Canada's Overall Comprehensive Wealth (Especially Compared with Other Leading Countries)

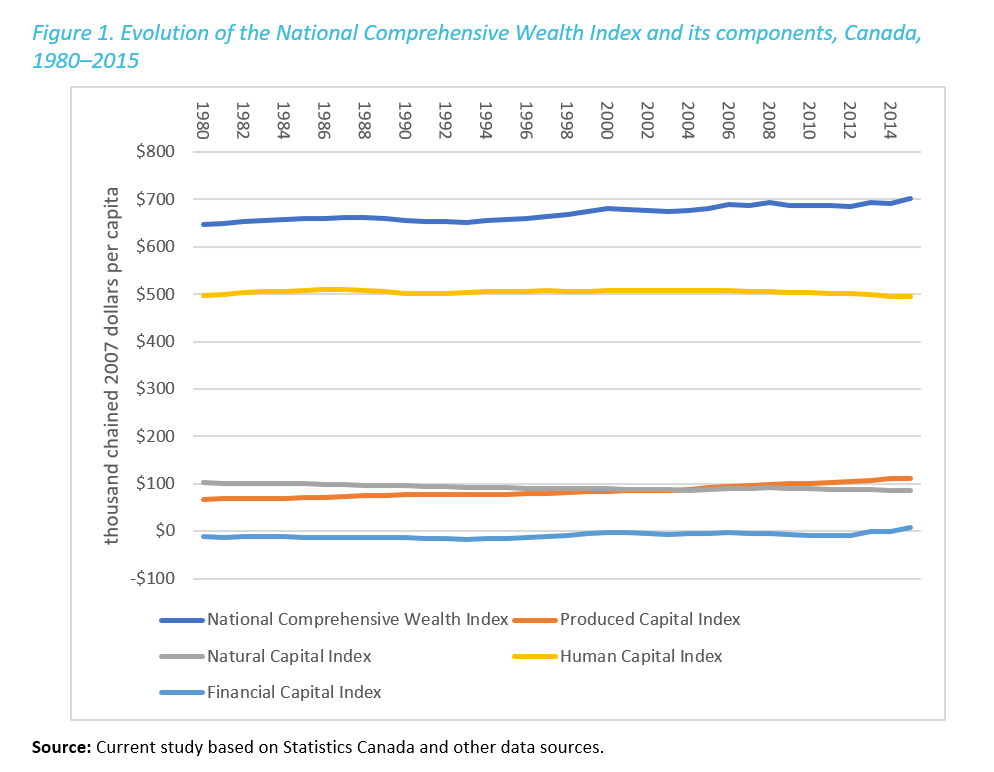

The value of Canada’s comprehensive wealth portfolio grew from $647,000 per capita in 1980 to $701,000 in 2015, an annual average growth rate of 0.23 per cent (Figure 1). In contrast, GDP grew at an annual average rate of 1.31 per cent over the same period. In other words, GDP grew more than five times faster than the wealth foundation on which it rests.

Viewed through the lens of comprehensive wealth, then, Canada’s development has been far less impressive than GDP alone suggests.

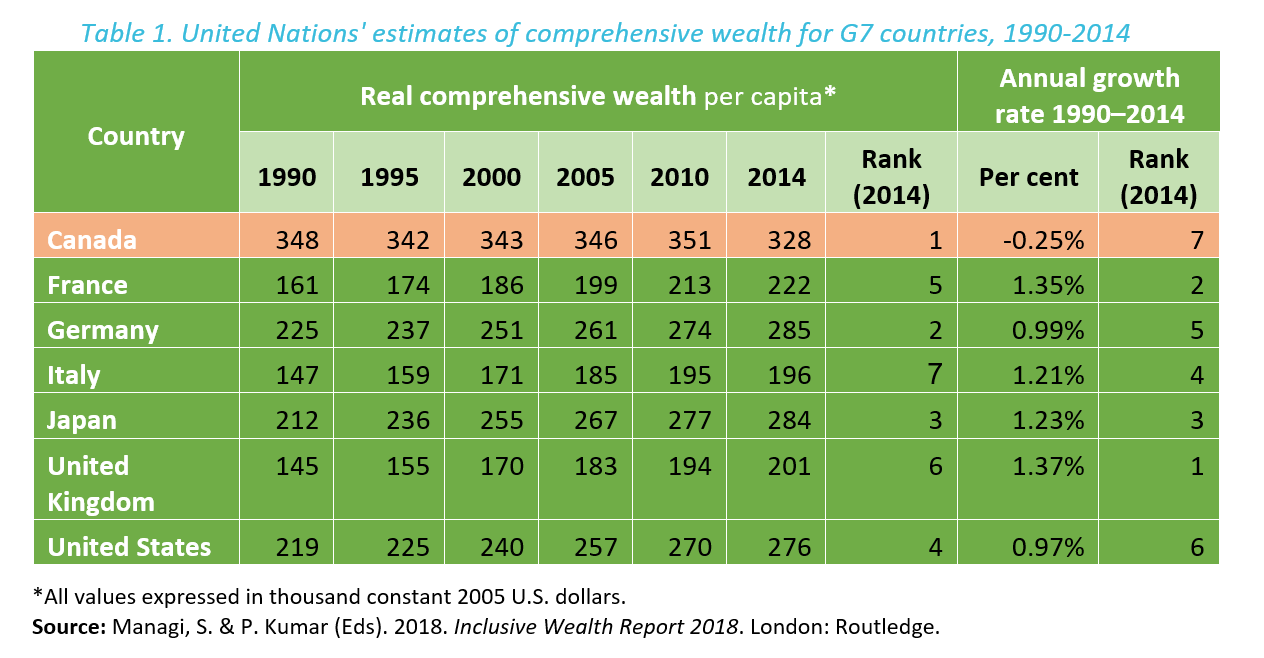

Moreover, according to the UN, Canada’s comprehensive wealth performance has been the worst among G7 countries in recent decades.

Canada is fortunate to be wealthy compared with its peers. In a 2018 global study on comprehensive wealth (based on methods broadly consistent with those here), the UN ranked Canada first among G7 nations in terms of the level of comprehensive wealth per capita. Its position at the top of this list was due largely to its reserves of natural capital, an advantage that puts the country in a position of clear strength vis-à-vis its peers. Canada had nearly four times more natural capital than the next closest of its G7 peers (the United States) in 2014.

At the same time—and consistent with the findings of this study—the UN ranked Canada last among G7 members in terms of the growth in comprehensive wealth. By the UN’s estimates, Canada’s comprehensive wealth actually fell between 1990 and 2014 (by 0.25 per cent annually on average), whereas that of every other G7 nation grew substantially (Table 1).

Clearly, other countries are doing better than Canada at ensuring the growth of their comprehensive wealth portfolios—and they’re catching up to Canada’s level as a result. In 1990, the average comprehensive wealth in other G7 countries was 53 per cent of Canada’s; by 2014, this share had climbed to 74 per cent. At current rates of growth, the UN’s findings suggest Canada will lose its first-place position to Japan in 2024 and will fall to fifth place in less than a generation (2039).

2. Canadian households have taken on unprecedented levels of debt since 1980.

Canadians are shifting their investments toward housing and away from financial assets, inflating house prices and leaving the rest of the economy reliant on foreign lenders for nearly three quarters of investment flows after 2012. The last time the Canadian economy relied on foreign sources for such a large share of investment was in the mid-1960s.

3. Climate change has emerged as a major threat to Canada’s comprehensive wealth portfolio.

Climate change threatens comprehensive wealth, particularly extremes of heat, cold, precipitation and wind. Flooding, wildfires and tornadoes—and the damage they cause—are all on the rise

The Insurance Bureau of Canada reports insurance payouts due to extreme weather events have doubled every five-to-ten years since the 1980s. Six straight years of insurance losses exceeding $1 billion were witnessed in Canada from 2009 to 2014. In contrast, insured losses averaged only $400 million a year between 1983 and 2008 and only two years saw losses exceeding $1 billion.

With $3.4 billion in payouts due to floods in Alberta and Toronto, an ice storm in eastern Canada and other extreme weather, 2013 was a record-breaking year. It was surpassed, however, by a single event in 2016—the Fort McMurray wildfire. That fire is estimated to have caused $3.58 billion in insured property losses. It was by far the largest single payout for a natural disaster in Canada, more than doubling the $1.74 billion figure for the Alberta floods in 2013.

Since then, there has been severe flooding in Quebec in the spring of 2017 and massive wildfires in the interior of British Columbia that summer. Spring 2018 brought a record-setting flood to the Saint John River in New Brunswick and severe flooding to interior British Columbia. This was followed by a second consecutive summer of damaging wildfires in British Columbia plus extreme heat in Ontario, Quebec (where dozens of deaths occurred) and much of the rest of the country. Fall 2018 saw an unprecedented tornado event in eastern Ontario and western Quebec, with major damage to homes and infrastructure.

4. Produced capital concentration.

Canada’s investments in produced capital (like buildings and machinery), while growing substantially over the period, became increasingly concentrated in just two areas: housing and oil and gas extraction infrastructure. By 2015, 25 per cent of all business-sector produced capital was invested in oil and gas extraction assets—up from 9 per cent in 1980.

In addition to these main areas of concern, we find other areas of weakness in the country’s comprehensive wealth portfolio.

- Canada’s largest and most important asset—its human capital—did not grow at all from 1980 to 2015. In fact, the average Canadian held just slightly less human capital in 2015 ($496,000) than in 1980 ($498,000). This raises questions about how well equipped the workforce is to deal with the challenges faced by the economy: low productivity growth, the need for innovation and economic diversification and U.S. protectionism, to name a few.

- Canada’s market natural assets (minerals, fossil fuels, timber, agricultural land and built-up land), traditionally a backbone of the country’s wealth, declined by 17 per cent from 1980 to 2015 as a result of depletion of many of Canada’s natural resources.

- The value of Canada’s oil and gas assets fell by 83 per cent in 2015 on the heels of the drop in oil prices. While oil prices are notoriously volatile (and have since regained some of their losses), current trends in global energy markets suggest oil prices are likely to trend downward in the long term, raising the risk of stranding some of Canada’soil sands assets, which (as noted) represent 25 per cent of business-sector produced assets.

- Canada’s key ecosystems—forests, wetlands, grasslands and lakes/rivers—declined in physical extent (though modestly in comparison to their size) and became increasingly impacted by human development.

In a positive trend, Canada’s financial capital grew rapidly, especially in recent years. For likely the first time in history, Canadian ownership of foreign financial assets outstripped foreign ownership of Canadian assets in 2015. These gains were, however based on unusually favourable market trends—especially unprecedented growth in the U.S. stock market and the declining value of the Canadian dollar—rather than on actual investments.

As for Canada’s social capital, it appeared to hold steady over the period. Diversity in social networks and trust in institutions showed steady increases, while voter turnout in federal elections generally declined (rebounding somewhat in the two most recent elections). Other social capital indicators showed little change in either direction over the period.

The overall trends in the country’s comprehensive wealth portfolio are summarized in Table 2. As a result of these trends, we believe Canada’s comprehensive wealth portfolio—and Canadians’ long-term well-being—could suffer additional losses from relatively small changes in economic, environmental or social conditions. The most likely of these—rising interest rates and a cooling of the housing market—began to play out at the end of 2017 with consequences yet to be determined.

How Would Comprehensive Wealth Measures Help Ensure Sustainability of Well-Being?

While Canadians clearly feel intuitively their long-term well-being is under threat, they do not have the information they need to confirm their concern. This is because comprehensive wealth is not measured in Canada today. Some pieces of the portrait are available from Statistics Canada, but a complete, regular and clear assessment is missing.

In contrast, Canadians are fed a regular and rich diet of short-term statistics like GDP—monthly, quarterly and annually—and the media devote a lot of time and space to reporting them.

We believe Canada—and all countries—must begin measuring comprehensive wealth to balance the short-term view of development offered by GDP. With comprehensive wealth to use as another lens on progress, Canadians would know with confidence whether their well-being was on a sustainable path—and they would be able to hold their leaders accountable. Just as importantly, decision-makers would have a new tool to guide decision making, ensuring impacts on long-term well-being were considered alongside traditional short-term concerns like GDP growth. Today, the decision-making scales are tipped in favour of the short term. We believe it is time they be balanced.

Comprehensive wealth measures—if they were regularly available in Canada—would focus decision-maker’s attention on issues that we believe receive less attention than they deserve. Most obviously, they would draw attention to the impact of policies and projects on the assets that make up the comprehensive wealth portfolio. This alone is a significant strength. Wealth, in spite of its importance in assessing sustainability, receives far less attention today than GDP and other short-term measures.

By focusing on assets, which are long-lived, comprehensive wealth measures would draw attention to the long-term impacts of policies and projects. These can often be overshadowed by short-term benefits. Jobs, for example, can be both short- and long-term and the impacts of each are quite different. Creation of short-term, relatively low-wage jobs in construction, for example, is not as advantageous in the long run as creation of permanent jobs in, say, advanced manufacturing.

Similarly, investments in capital-intensive projects, may have large and positive impacts on GDP in the short term but can lock economic development into a specific path for many years to come. This may be fine if the long-term prospects for that path look good but less so if the investments are in a mature industry facing disruption from rapidly emerging technologies.

Another benefit of comprehensive wealth is the coherent framework it offers for assessing the diverse issues that can be associated with policies and projects. Issues ranging from job creation to natural resource revenues, ecosystem health, investment flows, debt and social development can all be assessed by considering their impacts on the various elements of the comprehensive wealth portfolio.

The basic decision-making criterion of the comprehensive wealth framework is that the value of the assets that make up the portfolio (and, therefore, the size of the portfolio itself) must be stable or increasing in per capita terms for development to be sustainable. Applied in the context of decision making, this means a policy or project should be evaluated based on its projected effect on the value of the comprehensive wealth portfolio. Projects/policies that maintain or increase per capita comprehensive wealth should be considered desirable and those that do not should be considered undesirable.

Beyond the effect on asset value, applying the comprehensive wealth lens leads to a focus on two other dimensions of assets: their diversity and their distribution.

Asset diversity is important for the resilience of wealth and well-being. Just as financial advisors counsel individuals to diversify their stock and bond holdings as a hedge against collapse in one part of their portfolios, nations also require asset diversification. Concentration of assets in one category of capital can lead to fragility and risks to sustainability.

Distribution of assets matters for reasons beyond diversity. Whereas diversification is the classic hedge against having“all your eggs in one basket,” concern about the distribution of wealth has more to do with ensuring fairness in economic and social opportunities across groups or regions.

Comprehensive Wealth Could Drive Better Decision Making

in Key Areas

A few areas our findings suggest greater focus on the long term would be beneficial and a comprehensive wealth lens would help.

Human capital

As in all developed countries, human capital is Canada’s most important asset, accounting for some 80 per cent of comprehensive wealth according to our findings. Yet, despite its importance, human capital is not regularly measured in Canada. It remains largely invisible to the public and decision-makers as a result.

As noted above, human capital did not grow in Canada from 1980 to 2015. The reasons for this are not fully clear. Aging of the population certainly played a part, though other countries with aging populations have managed to increase their human capital. The concern is amplified by the fact that the trend in human capital was weakest among young workers. Since young workers eventually take over from older workers, it is essential that they not have lower human capital than those they replace. It would be all too easy to allow this to happen, as early life experiences do much to shape later success. As the Governor of the Bank of Canada has said, a long period of unemployment for a young worker can leave a scar that lasts “a lifetime.”

Climate change

Climate change is one of the most serious threats to well-being in Canada and globally. It has the potential to disrupt nearly every aspect of the economy, the environment and society. Viewed through the comprehensive wealth lens, climate change poses particular risks to natural capital but threatens the value of produced, human, financial and social capital as well. We therefore strongly support current federal and provincial efforts to price carbon as part of Canada’s contribution to the Paris agreement on climate change.

Even if the global community succeeds in its Paris goal, however, the world is committed to some warming. That is why we believe more effort is needed to protect Canada’s comprehensive wealth portfolio from losses due to the impacts of climate change. Infrastructure such as transportation networks, ports and buildings needs to be designed and built with flooding and other extreme weather in mind. Crops need to be developed not for today’s rainfall patterns but those of the future. Cities need to be prepared to deal with wider extremes of heat and cold for their vulnerable populations.

Comprehensive wealth measures would help here by both tracking climate-related variables and by revealing more fully the impacts of extreme weather on Canada’s comprehensive wealth portfolio.

Diversification of natural and produced capital

Our analysis reveals two areas where there was substantial concentration of Canada’s comprehensive wealth portfolio between 1980 and 2015: market natural capital and produced capital. In the case of market natural capital, Canada’s sub-soil asset mix moved away from a broad suite of minerals and conventional fossil fuel assets toward a focus on oil sands and potash. Concentration on just a few resources is questionable for any country, but particularly one for which resource development has traditionally been so important. It is all the more questionable given current trends in global energy markets, with Canada’s oil sands facing supply-side competition from rapid growth in U.S. oil and gas production and renewables and weakening growth in fossil fuel use on the demand side.

Household saving and lending

Prior to 1997, the Canadian household sector routinely saved enough that it was able to lend to other parts of the economy. Since then, the sector has routinely spent all of its disposable income—and then some—leaving the majority of lending in Canada to come from non-residents. Excessive borrowing from foreign lenders worsens Canada’s financial capital situation and lowers comprehensive wealth, other things being equal.

As the household sector reduced its saving rate, it also changed its investment focus, putting more of its eggs in the real estate basket and fewer in financial assets such as stocks and bonds. Not only did this reduce household liquidity—a concern now interest rates have begun to rise—but it also shifted investment away from relatively more productive assets like corporate equities.

Social capital

Social capital is arguably the most complex and least understood element of the comprehensive wealth portfolio. It is also facing wide-ranging pressure today, as traditional concepts of family, community and nationhood are challenged and reinvented, fueled by the instantaneous flow of information and ideas of the information age. The need to measure social capital has never been greater. While Statistics Canada already measures some of its elements, the data it reports are infrequent and incomplete.

Canada is fortunate to have some of the most respected social capital researchers in the world. These experts are making good headway in defining and measuring social capital and understanding its role as a form of wealth. Committing to regular measurement of comprehensive wealth would give their work the attention and support it deserves.

An Opportunity for Canada to Lead

Of course, simply publishing estimates of comprehensive wealth would do nothing to assure the sustainability of Canadians’ well-being. The measures would have to be used to guide decision making, just as GDP and other indicators are used today. With comprehensive wealth measures in place, decision-makers would have a more balanced perspective on progress. No longer would short-term income growth be the default focus of attention. It would be complemented by an equally important focus on the asset base underlying Canadians’ well-being.

Fortunately, Canada is better positioned than any other nation to show leadership on the measurement of comprehensive wealth. Statistics Canada—already a world-class organization—measures more of the components of comprehensive wealth than any other statistical agency. Its measures of produced and financial capital are excellent as they stand. It has sound—if not fully complete—measures of natural capital that could be readily augmented.Its experimental measures of human capital could also be readily turned into official measures. Many elements of social capital are captured in its various household surveys and these could be brought together into more cohesive statistics.

We believe the federal government should fund Statistics Canada to carry out the needed changes to its programs and begin regular reporting on comprehensive wealth, just as it has long done with GDP. Doing so would require a relatively modest investment on the government’s part but would pay major dividends for the nation.

It would help Canadians better understand their future prospects. It would better equip leaders to make balanced decisions. And, not least, it would put Canada in the position of leading on the G7’s call to go beyond GDP and measure what matters in the long term for prosperity and well-being.