Country profile: petroleum-product subsidies in India

In 2009, 32% of India’s primary commercial energy consumption was derived from petroleum (BP, 2010) and almost 79% of the domestic crude oil demand was met from imports (TERI, 2010). According to current estimates, this percentage will increase to 91% by 2030/31 (TERI, 2009).

Until the late 1990s, the country’s fuel prices were controlled by the government through a policy called the Administered Pricing Mechanism (APM). Despite dismantling the APM, and ambitions to entirely liberalize prices between 1997 and 2002, subsidies on four sensitive products were never given up for long – Motor Spirit (MS), High Speed Diesel (HSD), domestic liquefied petroleum gas (LPG) sold to households, referred to in India as ‘domestic LPG’, and Superior Kerosene Oil (SKO) targeted to the poor through the country’s public distribution system (PDS), commonly referred to as ‘PDS kerosene’. Subsidies to these products were particularly costly in the period after 2004, when rising international crude oil prices led the government to introduce a price-band mechanism and thereafter ad-hoc pricing mechanisms.

Various expert groups and government-appointed committees have, from time to time, suggested that the prices of these products be decontrolled. The government, however, has only ever partially implemented the recommendations of these expert groups and was never able to fully decontrol the final retail prices of these products. The latest in this series of efforts took place in June 2010, following the recommendations of an expert group headed by Dr. Kirit S. Parikh (GoI, 2010), when the government decided to decontrol the price of petroleum products and as a first step deregulated the price of petrol. An in-principle decision was also taken to liberalize diesel prices at some unspecified future date.

Further action, however, has not yet taken place, with the government continuing to control the price of diesel, domestic LPG and PDS kerosene, and seeming to waver on its commitment regarding petrol. In the last few months, even as international crude prices rose by more than 12% between January and March 2011, it was only on 15th May that the prices of petrol were raised by INR 5 (US$ 0.1) per litre thereby taking the prices of petrol to INR 63.37 (US$ 1.4) per litre in Delhi (prices vary across states, mostly due to differential tax structures).

Current pricing and subsidy regime

The Indian government controls prices by requiring downsteam companies, commonly referred to as Oil Marketing Companies (OMCs), to sell petroleum products at below-market prices. This, of course, results in ‘under-recoveries’ – which the Rangarajan Committee (GoI, 2006) defines as “the difference between the cost price and the realized price”. Here market prices refer to import trade parity prices that reflect the costs that would be incurred if the refined products were being imported rather than being refined and marketed domestically.

These financial losses are paid for in three main ways:

- First, the government has a scheme of providing budgetary subsidies on the sales of domestic LPG and PDS kerosene, equal in 2009-2010 to INR 22.58 (US$ 0.50) per cylinder of LPG and INR 0.82 (US$ 0.02) per litre of kerosene. In addition to this, a sum of INR 220 million (US$ 5 million) was also provided to lower the cost of freighting these products to remote areas under the Freight Subsidy (For Far Flung Areas) Scheme introduced in 2002. The total budgetary subsidies in 2009-10 were INR 27,920 million (US$ 624 million).

- Second, until 2008-09, the government also provided off-budget assistance in the form of special bonds called ‘oil bonds’ that were issued to OMCs. These were issued in tranches over the course of a financial year and accounted as income in the OMCs’ profit and loss statements. Interest rates were set anywhere between 6% and 9% and the bonds were given a period of maturity of up to 20 years. Since only their interest payments are accounted for as spending in the budget, oil bonds do not have any significant fiscal impacts at the point of issue. However, once the bonds are due, the repayment costs will have to be met from budgetary allocations. In the last two years, the government has not issued any oil bonds, with the finance minister having declared in his 2010-11 budget speech that no further oil bonds will be issued and that any subsidies allocated to the sector will from now on be explicitly met from budgetary allocations.

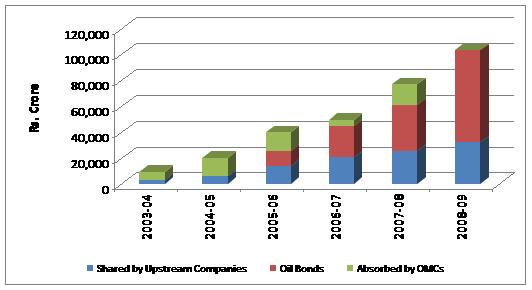

- Third, the government has forced some proportion of the losses to be absorbed by the oil industry. For example, the recent budgetary allocations for LPG and kerosene have been too low to cover the difference between the actual and realized price, such that in 2009-10 marketing companies had to bear under-recovery costs of INR 14.85 (US$ 0.33) per litre of kerosene and INR 178.13 (US$ 4.00) per cylinder of domestic LPG. One variant on this option has been to direct upstream oil companies to sell their crude to OMCs at discounted rates, thus sharing the burden more widely across the industry. In 2008-09 and 2009-10, upstream companies contributed a total of INR 320 billion (US$ 7.2 billion) and INR 144.3 billion (US$ 3.2 billion), respectively, as assistance to the OMCs. The sharing of the under-recoveries between oil bonds and industry actors is as shown in the figure below.

Sharing of under-recoveries by oil companies

Source: GoI, 2010. Note that ‘crore’, the unit of measurement on the y-axis, is equal to 10,000,000.

Over time, the share of costs met by budgetary subsidies has declined, whereas the difference between the actual price and the realized price of subsidized products has increased. According to recent estimates by the Petroleum Planning and Analysis Cell (PPAC), a government appointed agency responsible for collecting information related to oil companies, firms are currently incurring a daily under-recovery of INR 4.45 billion (US$ 0.1 billion) on the sale of subsidized diesel, kerosene and LPG (PPAC, 2011).

It should be noted that the government controls the prices of only the National Oil Marketing Companies and therefore the subsidies are also allocated to only these companies. Although private companies are free to charge import-parity based prices, in reality they struggle to compete against the sales of subsidized fuel. There is currently only very limited participation from these private companies in marketing oil products.

Impact of subsidies

The two major impacts of the subsidies are on consumers and the fiscal situation of oil companies and the Indian government.

At the level of consumers, subsidies can lead to a number of perverse outcomes. Kerosene, for example, is mostly used for lighting in rural households, despite being an inefficient fuel for lighting. In case of automotive fuels, the pricing regime leads to wasteful consumption of fuel – indeed, the country’s shift away from public transport towards privately owned transport is essentially leading to an excessive and inefficient usage of fuel.

There are also questions of access for marginalized areas of society. A significant share of the subsidized kerosene actually gets diverted to the black market and is used to adulterate diesel (NCAER, 2005). And despite recent efforts to convert rural households to LPG-use, adoption of LPG remains limited. According the 64th Round of the National Sample Survey, only 9% of the rural households used LPG for cooking (NSSO, 2007), suggesting that many households are unable to avail themselves to the supposed welfare gains of cheap fuel.

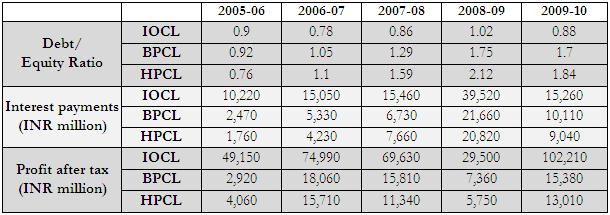

At the financial level, oil marketing companies have in the past few years suffered from a liquidity crunch because oil bonds are long term in nature and do not provide adequate cover in terms of short-term working capital requirements. Although the OMCs have from time to time sold parts of these bonds in the secondary market, the low interest rates and the fact that these have not been given a Statutory Liquidity Ratio (SLR) status – allowing banks to count them as part of their mandatory liquid reserves – reduces their marketability (IEA, 2010), such that companies have often sold them at discounted rates. This means that in times of high oil prices, oil companies have tended to experience a decline in profits, an increase in interest payments and a rise in their debt-to-equity ratios. These changes were particularly apparent in the period from 2006-07 to 2008-09, as illustrated in the table below.

Financial performance of the oil marketing companies

Source: Compiled from the financial statements of the respective oil companies,

IOCL: Indianoil Corporation limited;

BPCL: Bharat Petroleum Corporation Limited;

and HPCL: Hindustan Petroleum Corporation Limited.

The Debt/Equity Ratio has been calculated by using the formula: (Total Borrowings/Net Worth). where Net Worth is the sum of the Share Capital and Reserves and Surplus of the company.

The impact of oil subsidies is not limited to the downstream companies alone. Since upstream companies also share the burden of petroleum product subsidies, they have fewer funds available for investment in their core activities. The imposition of subsidies has also had an adverse impact on the level of competition in the sector as it has resulted in very limited private participation in the national market.

Finally, the subsidy regime also has an impact on government finances, because in the long-run the oil bonds will have to be repaid. Even in the short-run, as the government has decided to stop issuing oil bonds, it is likely that the burden of any future fuel subsidies would put significant pressure on India’s budgetary finances.

Possible interventions

As the aim of the subsidies is to improve the welfare of marginalized sections of society, the most direct intervention would be to better target the subsidy to reach this population. One proposal in this respect has been to link subsidy provision to India’s Unique Identification (UID) scheme, allowing subsidies to be individually targeted to unique identity numbers for each individual in the country. According to an interview in May with Planning Commission member Saumitra Chaudhuri, such reforms to food, fertiliser and fuel subsidies will be outlined in the approach paper to India’s 12th Five Year Plan (2012−17), though it remains to be seen how effective the measure will be in the times to come.

More strategic possiblities include reducing the need for fossil-fuel consumption. In the short term, this might take the form of safer and more reliable forms of public transport. In the long-term, research and development of alternative fuels and renewable sources of energy will help wean away the economy from excessive dependence on petroleum.

Anmol Soni is a Research Associate at the Energy and Resources Institute, TERI, New Delhi, India. She works on areas related to petroleum and natural gas in India.

This article draws on the larger work currently being conducted on subsidies on petroleum products by the Centre for Research on Energy Security, TERI.

References:

BP. (2010). BP Statistical Review of World Energy. British Petroleum. Available at: www.bp.com/.../bp.../statistical...review.../2010.../statistical_review_of_world_energy_full_report_2010.pdf

GoI. (2010). Report of the Expert Group on a Viable and Sustainable System of Pricing of Petroleum Products. New Delhi: Government of India.

GoI. (2006). Report of the Committee on Pricing and Taxation of Petroleum Products. New Delhi: Government of India.

IEA. (2010). India’s Downstream Petroleum Sector: Refined product pricing and refinery investment. Paris: International Energy Agency.

NCAER. (2005). Comprehensive Study to Assess the Demand and Requirement of SKO. New Delhi: National Council for Applied Economic Research.

NSSO. (2007). Household Consumer Expenditure in India, 2007-08 (NSS 64th Round). National Sample Survey Organisation, Ministry of Statistics and Programme Implementation, Government of India.

PPAC. (2011). Information on Petroleum Prices and Under-Recoveries. Petroleum Planning and Analysis Cell, Ministry of Petroleum and Natural Gas, Government of India. Available at: http://ppac.org.in/WRITEREADDATA/PS_oil_prices.pdf

TERI. (2010). TERI Energy Data Directory and Yearbook, 2010. New Delhi: The Energy and Resources Institute (TERI).

TERI. (2009). India’s Energy Security: New opportunities for a sustainable future, Paper submitted to Hon’ble Prime Minister of India. New Delhi: The Energy and Resources Institute (TERI).